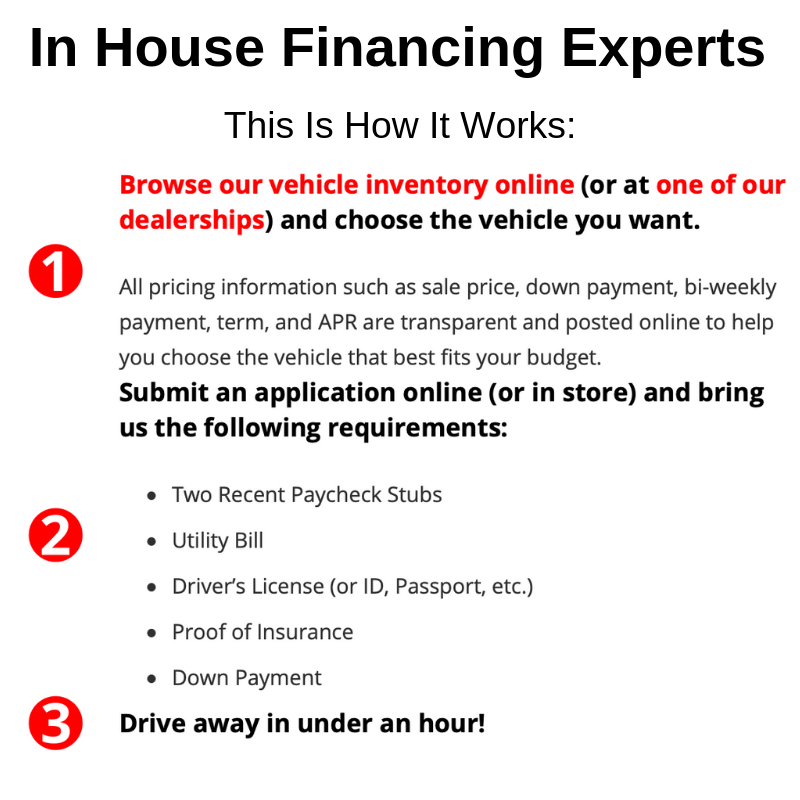

In-house financing requires applicants to provide proof of income and a valid government-issued ID. Credit history and down payment may also be necessary.

Navigating the world of in-house financing can feel like a daunting task, emphasizing the need for clarity and simplicity in the process. Financial institutions offering this service typically cater to clients who are seeking loans directly from the seller, such as car dealerships or furniture stores.

For many individuals, in-house financing presents an attractive option for making large purchases without having to secure funds from external lenders. By fulfilling specific requirements, customers can take advantage of a more streamlined and integrated borrowing experience. Understanding the prerequisites ensures a smoother transaction, fostering trust and confidence between buyers and sellers. It’s critical to enter these agreements well-informed, reinforcing the need for transparent and easily accessible information.

Credit: hesfintech.com

Essentials Of In-house Financing

Definition And Function

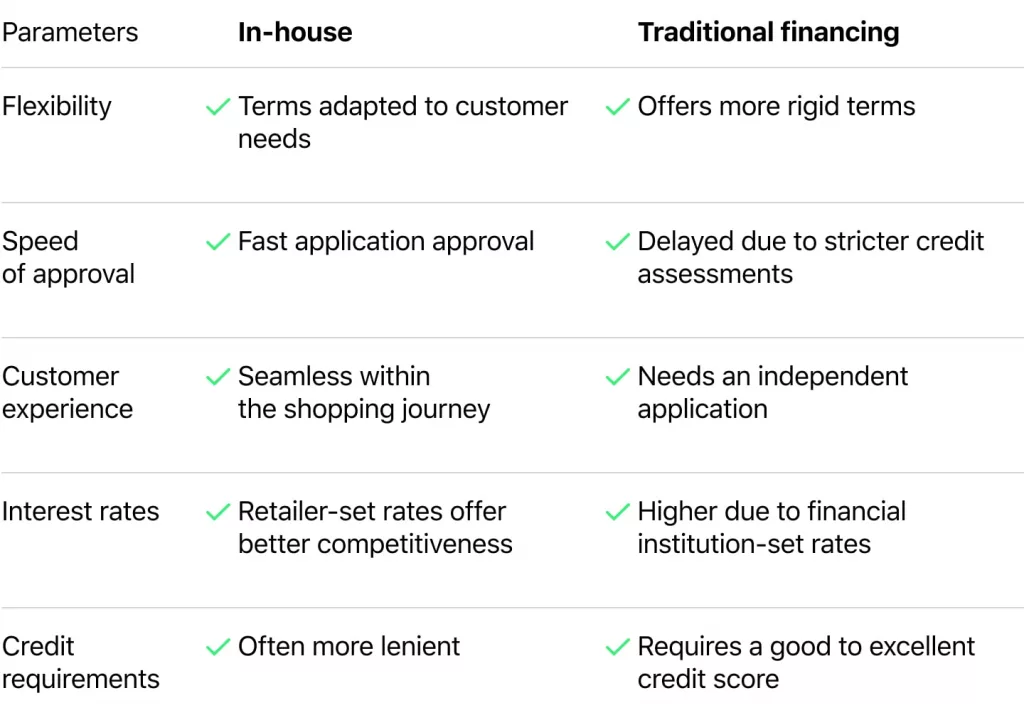

In-house financing happens when a company provides loans to its customers directly. Unlike bank loans, it cuts out the middleman. This arrangement allows customers to make purchases they otherwise may not afford upfront.Primary Benefits For Businesses And Customers

- Businesses enjoy increased sales, as financing makes their products or services more accessible.

- They gain customer loyalty through catered financing options.

- Customers benefit from a simplified transaction process with less paperwork.

- They receive flexible payment plans that suit their financial situations.

Credit: www.entrepreneur.com

Eligibility Criteria For Borrowers

Credit Score And History Considerations

Your credit score is a key factor. Lenders look at this three-digit number. It tells them about your past credit behaviors. A good score can mean better loan terms. Lenders may check your credit reports from major bureaus. They look for patterns in payment history and credit usage. A history of timely payments boosts your chances. High credit utilization or defaults may hinder your application. Yet, some lenders offer chances to those with lesser scores. High-interest rates often apply here.Income And Employment Verification Processes

Proving your ability to pay is essential. Lenders will ask for recent pay stubs. They may also require bank statements and tax documents. This proves you have a reliable income source. Your employment history is also under the lens. Long-term employment signifies stability. Lenders use this data to calculate your debt-to-income ratio. This shows your ability to handle new debt. A lower ratio is preferable. It means you have fewer obligations compared to your income. To summarize, have your credit information and income details ready. A strong credit score and stable income improve your likelihood of acceptance. Each lender will have unique standards. Prepare to meet these, and financing within reach becomes a reality.Business Considerations For Offering Financing

Assessment Of Financial Health

Before offering financing options, a business needs a solid financial foundation. Here are steps to assess this:- Analyze cash flow: Ensure the business has enough cash to cover loans.

- Review credit risks: Identify the risks of lending to customers.

- Check capital reserves: Keep funds to cover unexpected losses.

Legal And Regulatory Compliance

Understanding legal aspects is vital for in-house financing. Here are steps for compliance:- Know the laws: Federal and state laws must be followed.

- Find licenses needed: Some areas need a credit license.

- Maintain contracts: Legal contracts protect the business and client.

Administering An In-house Financing Program

Structuring Payment Terms And Interest Rates

Creating favorable conditions for both parties is essential. Companies should set clear, achievable payment terms for customers. To do this, a balance between competitive interest rates and business sustainability is vital. The terms must reflect:- Loan duration: Short-term loans may have higher payments but lower interest totals.

- Frequency of payments: Options can include monthly, bi-monthly, or weekly installments.

- Interest rates: Rates should be fair but also cover administrative costs and potential risks.

- Down payments: Initial payments can reduce risk and incentivize prompt repayment.

Managing Risks And Loan Defaults

Minimizing financial exposure is a priority. Strategies must be in place to tackle defaults. Key risk management steps include:- Customer screening: Assessing borrower reliability through credit checks can prevent issues later on.

- Clear contracts: Legal agreements should outline obligations and repercussions of non-payment.

- Reserve funds: Setting aside capital can help buffer lost income from defaults.

- Recovery actions: Defined procedures for handling late payments or defaults ensure consistent responses.

Credit: twitter.com

Frequently Asked Questions For In-house Financing Requirements

Is It Easier To Get Approved For In House Financing?

In-house financing often offers an easier approval process, especially for those with less-than-perfect credit, as dealerships may have more flexible criteria.

Do They Run Credit For In House Financing?

Yes, most in-house financing dealerships run a credit check to assess creditworthiness and determine loan terms.

What Is In House Financing Terms?

In-house financing terms refer to the loan conditions a company offers to customers directly without using a third-party lender. These terms include interest rates, repayment schedules, and down payment requirements, tailored by the seller to facilitate the purchase of their goods or services.

Conclusion

Navigating the terrain of in-house financing is pivotal for both businesses and customers. By understanding the typical requirements, borrowers can prepare effectively. Companies can offer clarity and build trust. Remember, clear documentation and financial stability are your keystones. Start the journey informed, and success in securing financing is more attainable.